Market Corrections are Healthy and Beneficial - they keep bubbles from forming – but only if you’re prepared

Last week's market declines are a good example of why it's never a good idea to follow crowds on Wall Street, especially during sharp downturns.

Panic-selling for long-term investors almost always ends poorly. Investors who stayed calm, followed their long term investing thesis and didn't panic during the financial crisis ended up recouping not only all their losses but also were still around to participate in the longest-running bull market in history.

This week, the market experienced a sharp downturn that has taken it lower from recent record highs set in September with the S&P 500 off roughly 7 percent in just the last few weeks. This took us back down to the lows of...wait for it...June!

However, investors earlier this year saw a similar scenario play out. Markets went into correction mode following an inflation scare in late January and early February. Soon after, though, a rebound took the market to new highs.

After the stock market’s historic growth that began in early 2009, many believe a 10% pullback may be a healthy thing. Such a drop is not horribly painful, by historical standards, and smart investors can cushion such a fall.

Market Corrections

Why is a market correction beneficial? Because it prevents another bubble from forming. Bubbles occur when stock prices get clearly out of line with the earning potential of the underlying companies. We saw the consequence of that in the awful 2000-02 and 2008-09 market wipeouts, when some people lost half their wealth or more.

Certainly, market corrections never feel healthy when they occur. People get fearful as the market declines, the media fan the flames by giving investors reason after reason to be afraid, and worries that this is the beginning of the next crash begin to develop.

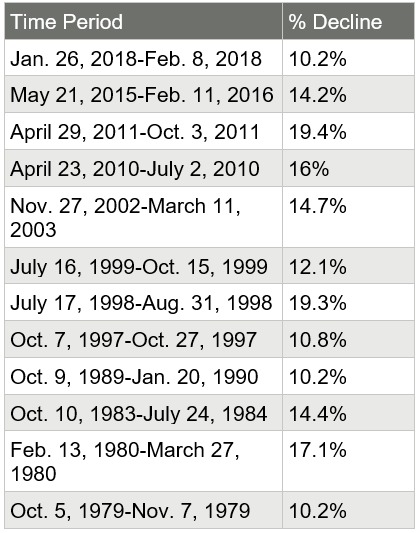

While many investors admit that a 5% pullback is manageably unpleasant, concerns expand when the market decline hits 10%. That’s what customarily constitutes a correction. In the late winter sell-off, from January 26th to February 8th of 2018, the Standard & Poor’s 500 index fell 10.2% leading the index to barely creep into correction territory. By early mid-summer, it had made up those losses, and then some, before powering on to new highs.

SMLXL

SMLXL

Ben Carlson, an institutional investment portfolio manager, looked at the S&P data going back to 1950, and found 28 instances when stocks fell by 10% or more. Thus, on average, the market has entered an official correction every 2.25 years.

S&P Losses of 10% or More Since 1950

Total Occurrences: 28 Times

Average Loss: -21.6%

Median Loss: -16.5%

Average Length: 7.8 Months

Greater Than 20% Loss: 9 Times

Greater Than 30% Loss: 5 Times

As you can see, the average post-1950 market correction lasted just under eight months and the median total loss was 16.5%. What about deeper declines? Of the 28 times the S&P 500 decreased by 10%, the market suffered a loss greater than 20% – the standard definition of a bear market – only nine times (32% of the time), and a loss greater than 30% only five times (18%). The data confirm that, although these types of large losses do occur, they really are the exception.

Here are the past 12 corrections in the S&P 500 Index, according to Standard & Poor’s:

SMXLL

SMXLLAre you thinking: “I don’t think I can stomach that median loss of 16.5%? Then that’s where the wisdom of diversification becomes apparent. Remember that the data above represent the historical performance of the S&P 500, an index composed of 100% stocks.

A capable fiduciary financial planner ensures you have an asset allocation mix of stocks, bonds and cash that represents your tolerance for risk. Consequently, your portfolio likely isn’t 100% stocks. In fact, the appropriate allocation for an average investor approaching or already enjoying retirement might be closer to only 50% stocks. This means that on average, your portfolio should decline only half as much as the S&P 500 during market downturns.

So, diversification brings the our sample investor endured, with a 50% stock portfolio, down to around 8.25% during the median decline. Are you now back in the “manageably unpleasant" range? If so, you likely have an appropriately constructed portfolio. If not, you may need to reevaluate your risk tolerance to ensure you are not exposing your nest egg to a larger loss than you can endure.

Although the recent market pullback might create anxiety, media headlines and possibly fear, remember this: we’ve been here before. Lastly, don’t fall for the media’s scare tactics. What we’re experiencing in the market is normal, don’t let them lead you to believe otherwise.

Tying it All Together

These are just a few things to keep in mind during any bout of market volatility. Sell offs happen in the stock market, as any seasoned investor knows, you just can’t let your emotions drive your investing decisions as trying to time the market is a fool’s errand. It happens far too often with people, and results in lost returns over time. As I often remind people, this is why its critical to have an investment approach and financial plan you can stick to through certain and uncertain times.

Does any of this bring up any additional questions? Things you hadn’t considered? Consider it an opportunity to reach out as I’m here to help!

Do you want to bring a new level of attention to your financial decisions? Reach out to me at ryanmohr@claritycapitalmgmt.com or schedule a complimentary consultation.

Sign up for Clarity Capital Management's Newsletter to stay on top of my blog posts and other communication

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation.