Clarity Capital Management Notables - May 2025

As promised, although the US stock market has rallied between our last Notables newsletter earlier this month, we wanted to provide some additional context to the investment and economic environment. Congrats on getting through the first quarter (phew!!).

Also: for Clarity Capital Management clients who have filed their taxes, we’d love to see them! Please remember to upload your return to the Vault.

Here’s our economic update:

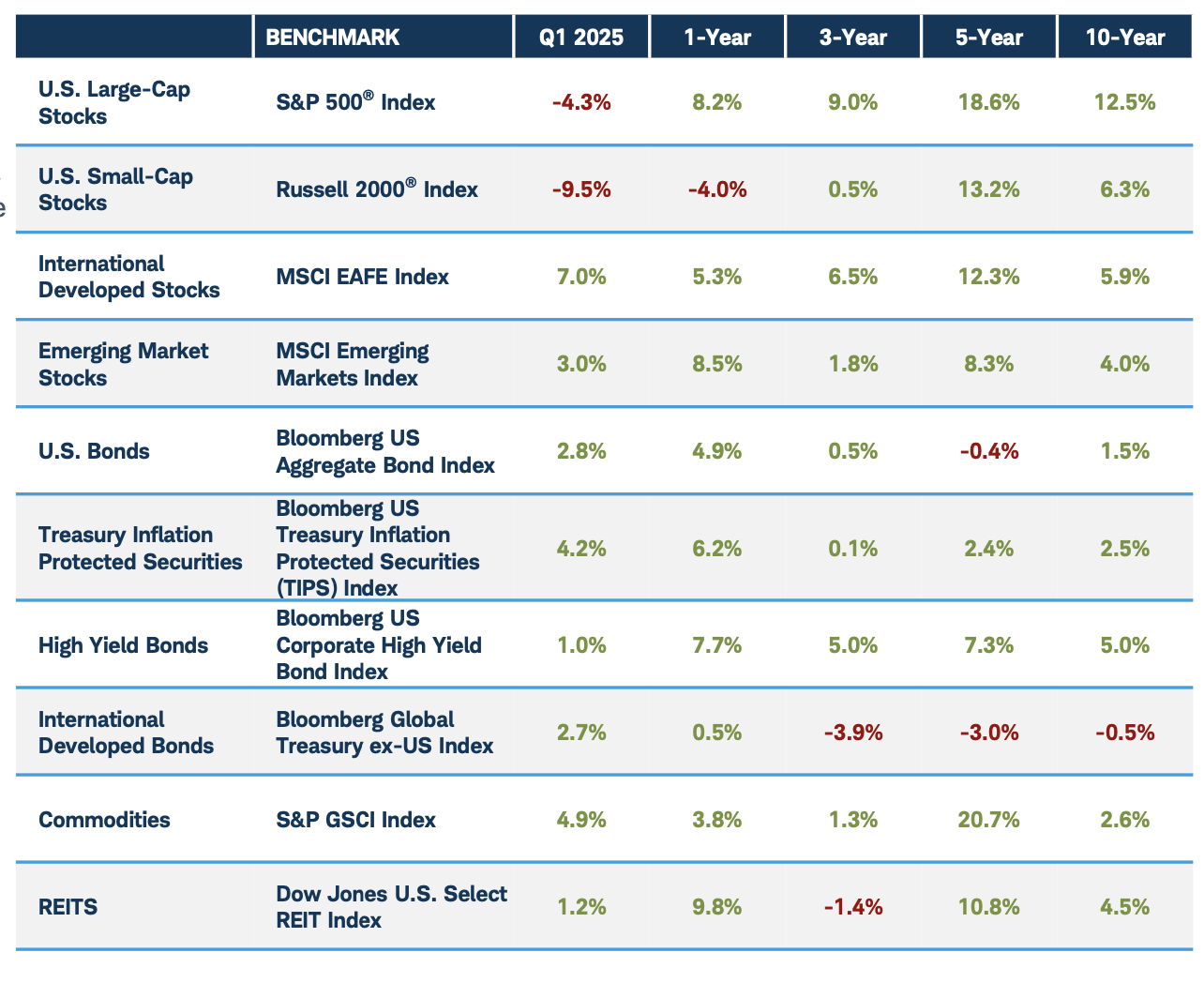

After closing out 2024 at record highs, U.S. equity markets encountered volatility in the first quarter of 2025. The year-end rally lost steam as inflation proved more persistent than expected, prompting the Federal Reserve to adopt a decidedly more hawkish tone. Hopes for multiple rate cuts faded, and renewed tariff threats only added fuel to the fire. Unpredictable actions by the U.S. government introduced additional uncertainty across investment and economic communities.

The tech-heavy NASDAQ and small-cap Russell 2000 both slipped into correction territory, as investor sentiment soured under the weight of persistent inflation, policy uncertainty, uneven corporate earnings, and disappointing economic data. GDP was revised downward, retail sales slowed, consumer confidence cratered, and the housing market showed mixed signs of strain.

For the first quarter of 2025, the S&P 500 fell 4.3%, the NASDAQ declined 10.3% and the Russell 2000 fell 9.5%. Meanwhile, global and international equity markets held up relatively well, with many international indices posting gains – offering a rare bright spot in an otherwise volatile quarter.

The erratic tone of U.S. trade policy continued to rattle nerves. The back-and-forth on tariffs clouded the outlook for global commerce and underscored the one thing Wall Street loathes most: uncertainty. There is a possibility that we’ve moved a bit past peak uncertainty concerning U.S. trade policy post the Presidential administration’s ‘liberation day.’ Even if true, the world is still likely far removed from anything resembling conviction as to where U.S. tariff rates and general trade policies will finally settle along with which countries and products could be impacted. As such, it’s likely market volatility remains higher than normal in the short-term.

We continue to believe that diversification is key to help managing risk and capturing returns across asset classes. Heightened volatility over the past quarter has helped prove that point. A globally diversified portfolio weathered the market storm better than most US equity indices. Looking ahead, continued political uncertainty surrounding the direction of US trade policy will likely drive markets, along with the trajectory of monetary and fiscal policy.